🌐 Hemispherical Stacks · 2026-03-21

🌐 Hemispherical Stacks — March 21, 2026

🌐 Hemispherical Stacks — March 21, 2026

Table of Contents

🎯 CSIS and Fortune Declare Data Centers "Front Line of Warfare" After IRGC Publishes 29-Target Hit List 🛰️ Chinese Satellites and BeiDou Navigation Enable Iran's Precision Strikes on Gulf Tech Infrastructure 🌊 Both Maritime Chokepoints Closed Simultaneously for First Time — Gulf AI Investments Trapped 🔌 Alcatel Submarine Networks Commits €100M to Expand European Cable Manufacturing Amid Global Vulnerability ⚡ Nvidia Cloud Partners Double Sovereign AI Factory Footprint as GTC 2026 Reveals $1 Trillion Pipeline 🔧 US Commerce Department Scraps Export Rule, Signals Tougher Performance-Based Chip Controls

---

🎯 CSIS and Fortune Declare Data Centers "Front Line of Warfare" After IRGC Publishes 29-Target Hit List

!Data Centers as Military Targets

{kind=link}

The Center for Strategic and International Studies published an analysis on March 20 declaring that "data is now the front line of warfare," following Iran's March 1 drone strikes on three AWS data centers in the UAE and Bahrain and the IRGC-affiliated Tasnim News Agency's publication of a 29-target hit list identifying AWS, Microsoft, Google, Oracle, Nvidia, IBM, and Palantir facilities across Bahrain, Israel, Qatar, and the UAE as "legitimate targets." Fortune's March 21 analysis explicitly states that corporations must now evaluate counter-drone and counter-missile defensive capabilities previously reserved for military installations.

The legal framework is uncharted territory. The Intercept's March 20 investigation quotes León Castellanos-Jankiewicz of the Asser Institute for International and European Law explaining that legality "turns on whether the specific facility, at the specific moment, is genuinely serving the military operations of a party to the conflict." The core problem is that US hyperscalers operate dual-use infrastructure: Microsoft runs the Pentagon's Joint Warfighter Cloud Capability on the same platform architecture serving civilian customers, and Amazon operates Pentagon-exclusive cloud regions sharing physical data center campuses with commercial services. Israel's March 11 strike on an Iranian data center containing IRGC salary data—disrupting military payments—confirms that both sides now classify compute infrastructure as legitimate strike targets regardless of civilian co-tenancy.

At the Stack level, the Cloud layer has become a battlefield. For two decades, data centers were treated as commercial real estate—insured like warehouses, secured against cyberthreats but not kinetic strikes. Iran's drone attacks and the 29-target list permanently reclassify them as dual-use military infrastructure subject to the same targeting calculus as munitions factories. CSIS draws a direct line from Ukraine's data-driven, AI-enabled warfare—made possible by Microsoft, Palantir, Clearview AI, and Starlink partnerships—to Iran's rational conclusion that destroying those companies' infrastructure is a legitimate military objective. When the Pentagon runs on AWS, attacking AWS is attacking the Pentagon. The cascading economic implications are as transformative as the military ones: Lloyd's of London does not currently price drone strikes against commercial data centers because until March 2026, that risk category did not exist. Reinsurance models, infrastructure bonds, and sovereign wealth fund investment theses for Gulf tech hubs all assumed cybersecurity risk, not kinetic destruction. Every hyperscaler data center in a conflict-adjacent region is now a military liability rather than a commercial asset—and the hemispherical stack is not just fragmenting along regulatory lines, it is militarizing at the Cloud layer in ways that connect directly to Chinese intelligence capabilities (see below) and the physical connectivity infrastructure now severed by the dual chokepoint closure.

---

🛰️ Chinese Satellites and BeiDou Navigation Enable Iran's Precision Strikes on Gulf Tech Infrastructure

!China-Iran Intelligence Cooperation

{kind=link}

The Small Wars Journal published a detailed analysis on March 20 documenting how Chinese intelligence infrastructure—satellite reconnaissance, BeiDou navigation systems, advanced radar networks, and electronic warfare technologies—has enabled Iran's precision targeting of US military installations and tech infrastructure across the Gulf. CIA Director John Ratcliffe told a Senate committee on March 19 that "the Iranians are requesting intelligence assistance from Russia, from China, and from other adversaries," while Iran's Foreign Minister confirmed receiving "military cooperation" from both countries. The convergence of these reports establishes that China's intelligence infrastructure is an active enabler of precision strikes against US tech facilities.

The analysis identifies four key dimensions of Chinese support. First, satellite intelligence: China's reconnaissance and signals intelligence constellation provides targeting data on data center locations and electronic emissions. Second, BeiDou navigation: China's GPS alternative offers precision guidance for Iranian missile and drone systems that cannot rely on US-controlled GPS during conflict. Al Jazeera reported on March 11 that BDS-3's military-tier B3A signal is "essentially unjammable," according to military analyst Patricia Marins—meaning strike guidance operates entirely outside US technical disruption capability. Third, Chinese-supplied radar helps Iran detect aircraft, drones, and naval vessels. Fourth, electronic warfare technologies enable signal jamming that degrades US defensive capabilities. The paper frames this within the 2021 China-Iran 25-Year Comprehensive Strategic Partnership.

At the Stack level, this reveals the Address layer (navigation, positioning, targeting) as strategically contested as the Earth layer (fabrication) or Cloud layer (compute). China's 56-satellite BeiDou constellation creates an alternative positioning infrastructure that renders US GPS denial ineffective against Iranian weapons systems. When data center coordinates are acquired via Chinese satellite intelligence and strike guidance provided via BeiDou, the entire targeting chain operates outside US technical control. The hemispherical stack bifurcation extends beyond chip fabrication and cloud platforms to who controls the positioning layer that determines what can be precisely destroyed. China is conducting infrastructure warfare against US tech assets without firing a single weapon—"Chinese eyes, Iranian missiles," as the Small Wars Journal frames it—a division of labor rendering bilateral deterrence frameworks obsolete.

---

🌊 Both Maritime Chokepoints Closed Simultaneously for First Time — Gulf AI Investments Trapped

{kind=link}

Rest of World reported on March 20 that the simultaneous closure of both the Strait of Hormuz and the Red Sea to commercial traffic represents an unprecedented event in the history of global connectivity: "Closing both choke points simultaneously would be a globally disruptive event. I'm not aware of that ever happening," said Doug Madory, director of internet analysis at Kentik. Iran declared Hormuz shut on March 3, threatening to "set ablaze" any vessel attempting passage, while Houthi militants announced resumed attacks on Red Sea shipping in solidarity with Iran. Together, these closures trap approximately 17 submarine cables in the Red Sea and additional cables through Hormuz—with specialized repair ships unable to access either passage.

The infrastructure consequences cascade. AWS told customers to consider migrating workloads out of the Middle East entirely after drone strikes damaged three facilities. Meta's long-term response is Project Waterworth, a 50,000-km cable designed to bypass the Middle East by connecting the US, India, South Africa, and Brazil. The 2Africa Pearls extension—scheduled to connect nine countries from Oman to India in 2026—now faces indefinite delay. CSIS's Sam Zabin noted that Gulf data infrastructure "has never been tested this way. Oil has had decades of conflict exposure and is heavily integrated into military planning. Data centers, until recently, were treated as commercial assets rather than national security concerns."

At the Stack level, this is the Address layer (submarine cable topology) fragmenting under Earth layer (territorial conflict) pressure. The global internet does not fail when both chokepoints close—it bifurcates. Traffic between Europe, Asia, and Africa that normally transits through the Gulf must reroute through Atlantic and Pacific paths designed for backup capacity, not primary load. The February 2024 precedent is instructive: when three Red Sea cables were severed by a dragging anchor from a Houthi-struck cargo ship, 25% of traffic between Asia, Europe, and the Middle East was disrupted, and one cable took five months to repair. With repair crews locked out of both chokepoints simultaneously, multiple failures could persist for the conflict's duration. US tech firms bet $100+ billion on Gulf data center investments without adequately assessing kinetic risk to the physical infrastructure connecting those facilities to global networks. The hemispherical stack's most expensive vulnerability is not chip fabrication or cloud capacity—it is the geographic concentration of cable routes through two narrow passages that a single conflict can close simultaneously.

---

🔌 Alcatel Submarine Networks Commits €100M to Expand European Cable Manufacturing Amid Global Vulnerability

!Alcatel Submarine Networks Expansion

{kind=link}

Alcatel Submarine Networks (ASN) unveiled a €100 million investment plan on March 18 to modernize its submarine cable manufacturing facilities in Calais, France, and Greenwich, UK, reinforcing European production capacity for the backbone infrastructure carrying 99% of intercontinental data traffic. The three-year initiative (2026-2028) is part of ASN's broader "Ambition 2030" strategy for next-generation cable technologies, coinciding with a submarine optical fiber cable market projected to grow from $18.1 billion in 2026 to $29.65 billion by 2032, an 8.53% CAGR driven by cloud computing, streaming, and AI workload expansion.

The timing maps directly to the dual chokepoint closure. With Red Sea and Hormuz inaccessible to cable repair vessels, demand has shifted from repair to replacement—new routes bypassing conflict-prone passages entirely. Meta's Project Waterworth (50,000 km, explicitly bypassing the Middle East), India's new Captive Telecommunication Services Rules enabling hyperscalers to build private "AI corridors," and the rerouting imperatives all represent demand that exceeds current manufacturing capacity. Submarine cable manufacturing is a bottleneck industry with only three major players: ASN (Nokia subsidiary, France/UK), SubCom (US), and NEC Submarine Networks (Japan). New cable routes require years of planning, permitting, and manufacturing—the infrastructure response to today's conflict won't be operational until 2028-2030 at the earliest.

At the Stack level, this is the Earth layer (manufacturing, physical production) responding to Address layer (cable topology) vulnerability. ASN is a Nokia subsidiary headquartered in Paris, with production straddling the Channel to maintain access to both EU and post-Brexit UK regulatory frameworks. The submarine cable market is shifting from traditional carrier consortia to a multi-stakeholder model where hyperscalers co-own the cables connecting their data centers—vertically integrating the Address layer with the Cloud layer and concentrating control over both compute and connectivity in the same corporate hands. The parallel with Nvidia's sovereign AI program is instructive: just as nations seeking compute sovereignty through NCPs remain dependent on a single US chip vendor, nations seeking connectivity sovereignty through hyperscaler-owned cable routes trade carrier dependency for platform dependency. Europe's position as the world's primary cable manufacturing hub gives it leverage over this vertical integration—but only if production capacity keeps pace with rerouting demands the Gulf conflict is generating.

---

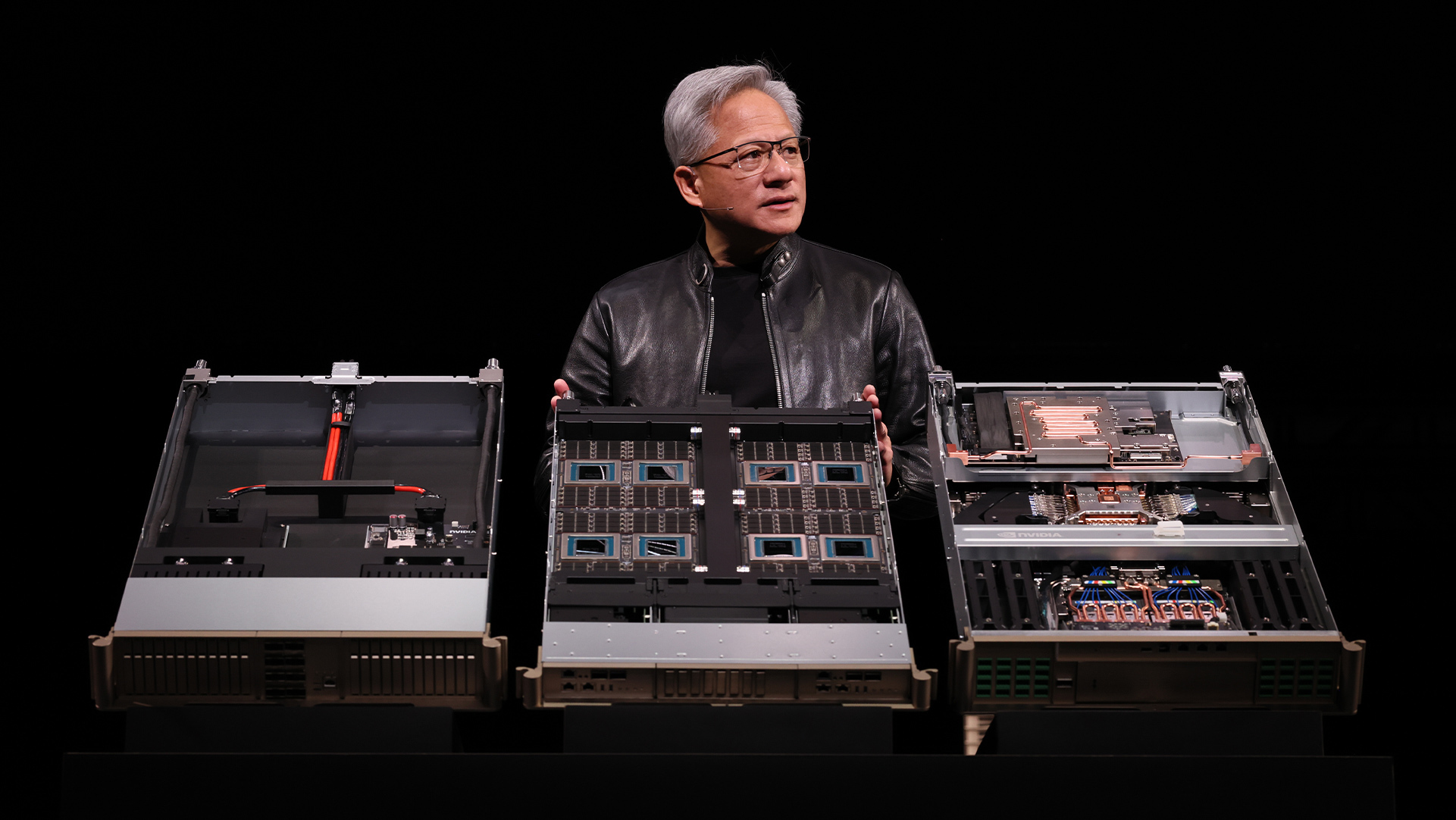

⚡ Nvidia Cloud Partners Double Sovereign AI Factory Footprint as GTC 2026 Reveals $1 Trillion Pipeline

{kind=link}

Nvidia's GTC 2026 conference concluded with announcements on March 20-21 that its Cloud Partners (NCPs) have doubled their AI factory footprint year over year, "advancing sovereign AI in the U.S., Australia, Germany, Indonesia, India and more." CEO Jensen Huang's March 16 keynote revealed the Vera Rubin architecture—comprising seven different chips and five dedicated racks that unify entire data centers into single AI factories—alongside a projected $1 trillion in chip orders through 2027 across Blackwell and Vera Rubin platforms. The Seoul Economic Daily characterized the transformation as moving "from chip maker to AI infrastructure giant," noting that GTC has evolved from a GPU developer conference into a sovereign compute summit where nations negotiate infrastructure access.

The "sovereign AI" framing is strategically calculated. Nvidia's NCP program places GPU infrastructure in countries seeking domestic AI capacity without depending on US hyperscaler clouds—directly addressing the sovereignty concerns that drive EU cloud policy (CISPE's anti-sovereignty-washing campaign), India's data localization ambitions, and Indonesia's digital infrastructure investments. The doubling of NCP footprint means more Blackwell GPUs are deployed in national AI factories operated by local partners rather than concentrated in AWS/Azure/Google data centers subject to US jurisdictional control. This creates a distributed Cloud layer where compute sovereignty is achieved through hardware placement rather than regulatory mandate—the infrastructure equivalent of NATO forward deployment.

At the Stack level, Nvidia occupies a unique position: controlling the Earth layer (chip design) that all other stack layers depend on, while simultaneously building the Cloud layer (sovereign AI factories) and defining the Interface layer (CUDA ecosystem lock-in). Vera Rubin's seven-chip, five-rack integration makes individual GPU deployments obsolete in favor of data-center-scale systems that only Nvidia can architect end-to-end. When a country buys sovereign AI capacity through an NCP, it receives not just chips but an entire infrastructure stack—power, cooling, networking, software—creating deep dependency on Nvidia's roadmap. The $1 trillion order pipeline represents not revenue alone but infrastructure lock-in across dozens of nations building compute sovereignty on Nvidia silicon. Sovereign AI factories create the distributed compute infrastructure that the Pax Silica alliance framework envisions—but every facility runs within CUDA's ecosystem, ensuring the silicon, architecture, and software remain US-controlled. The question: does this create genuine national capacity or merely relocate dependency from cloud platforms to hardware platforms?

---

🔧 US Commerce Department Scraps Export Rule, Signals Tougher Performance-Based Chip Controls

{kind=link}

The US Commerce Department withdrew a planned rule on AI chip exports while simultaneously signaling a tougher, revised framework linking export permissions to overseas investment commitments and strategic alignment, per Astute Group analysis published March 19. Commerce confirmed intent to "formalise a new approach to strategic AI accelerator export controls" targeting specific performance thresholds—interconnect bandwidth, compute density, memory bandwidth—rather than the Biden-era blanket licensing approach. Tom's Hardware reports the government targets "specific performance thresholds and end uses," while officials granted Samsung and SK Hynix 2026 licenses for chipmaking tool shipments to China—an annual approval system replacing the older waiver framework.

The policy shift creates deliberate uncertainty across the semiconductor supply chain. Procurement timelines for advanced AI hardware—particularly H100-class accelerators and custom ASICs manufactured on advanced nodes in Taiwan and South Korea—now face a "moving compliance target" where designs may deliberately limit interconnect speeds or memory bandwidth to fall below regulatory thresholds. The Astute Group notes that "orders placed under previous assumptions about export eligibility may now require reassessment, particularly for shipments destined for the Middle East and Southeast Asia." The Diplomat reported on March 18 that export curbs are "clouding South Korea's chip outlook"—revocation of Validated End-User status for Samsung and SK Hynix threatens the viability of their Chinese fabrication facilities, potentially forcing these Pax Silica allies to choose between maintaining Chinese operations and accelerating US-incentivized reshoring.

At the Stack level, this is the User layer (governance, export regulation) creating instability at the Earth layer (chip fabrication, hardware distribution) that cascades upward. Performance-based thresholds represent more granular export control but create a cat-and-mouse dynamic where chip designers optimize architectures to stay just below regulatory ceilings—exactly what Nvidia did with the A800 and H800 for the Chinese market under Biden-era rules. The shift acknowledges that the meaningful variable is not who buys the chip but what the chip can do—yet enforcement becomes exponentially harder when every accelerator must be evaluated against moving performance benchmarks. The irony connects directly to Nvidia's sovereign AI program: nations want sovereign compute precisely to hedge against this regulatory instability, yet the factories themselves depend on the same export-controlled hardware whose availability Washington keeps redefining. Export controls designed to restrict Chinese AI capacity simultaneously disrupt allied supply chains—the paradox at the heart of Pax Silica's governance architecture.

---

🔮 Implications: Infrastructure War Doctrine, Chokepoint Topology, and the Sovereign Compute Arms Race

The past 36 hours crystallize three structural shifts that will define hemispherical stack competition for the next decade: the formal emergence of infrastructure war doctrine, the exposure of chokepoint topology as the stack's greatest vulnerability, and a sovereign compute arms race that paradoxically deepens dependency on US chip design.

Infrastructure war doctrine is no longer theoretical. The IRGC's 29-facility hit list, CSIS's declaration that "data is now the front line of warfare," and Fortune's call for corporate counter-missile defenses collectively establish dual-use data centers as military targets—not as a future possibility but as current operational reality. What distinguishes this from historical infrastructure targeting (oil refineries, power grids, communications hubs) is the dual-use entanglement: the same compute infrastructure serving Pentagon weapons targeting also processes civilian commerce, health records, and financial transactions. The China-Iran intelligence pipeline compounds this: when Chinese satellite reconnaissance and BeiDou navigation provide the targeting chain for Iranian missiles, a data center's survivability depends not on physical hardening but on whether adversary alliance networks can locate it with precision. The Address layer has been weaponized against the Cloud layer through a third party's intelligence apparatus—a tripartite infrastructure warfare model that existing bilateral deterrence frameworks cannot address.

Chokepoint topology has shifted from theoretical risk to active infrastructure failure. Simultaneous Hormuz-Red Sea closure creates routing fragmentation that advantages countries with diverse cable paths (US, UK) and punishes those dependent on Gulf transit (India, East Africa, Southeast Asia). Alcatel's €100M manufacturing expansion and Meta's Project Waterworth represent permanent rerouting that accepts the Middle East is no longer a viable connectivity hub. The hemispherical stack's physical topology is being redrawn by missiles, not regulation—and the manufacturing bottleneck (three global cable producers, repair fleet nearing 65% retirement by 2040 per UNIDIR) means the infrastructure response to today's conflict won't arrive until 2028-2030.

The sovereign compute arms race is the deepest paradox. Nvidia's doubled NCP factories appear to deliver national AI sovereignty, but every facility runs on Nvidia silicon within the CUDA ecosystem, tethered to a single US vendor's roadmap and Washington's shifting export control regime. The $1 trillion order pipeline represents distributed dependency, not independence. The convergence—infrastructure war, chokepoint fragmentation, sovereign compute dependency—reveals a stack simultaneously militarizing, physically fragmenting, and economically consolidating. The question is no longer "where should we build?" but "what survives?"

---

📚 Research Papers

1. Sovereign AI: Rethinking Autonomy in the Age of Global Interdependence — Gupta et al., arXiv:2511.15734 (November 2025) - Key finding: Develops a formal framework treating sovereign AI as a continuum rather than binary condition, with policy heuristics for balancing autonomy across four pillars (data, compute, models, norms). Applied to India and the Middle East. - Link: https://arxiv.org/abs/2511.15734

2. Sovereign AI-based Public Services are Viable and Affordable — Ferrara et al., arXiv:2603.01869 (March 2026) - Key finding: Demonstrates through empirical experimentation that sovereign alternatives to global AI oligopoly providers are technically feasible and economically sustainable, challenging assumptions about general-purpose architecture dominance. - Link: https://arxiv.org/abs/2603.01869

3. The Dangerous Rise of Dual-Use Objects in War — Hathaway, Khan & Revkin, SSRN:4938707 (September 2024, revised June 2025) - Key finding: Analyzes how dual-use infrastructure proliferation erodes international humanitarian law protections, with direct implications for data center targeting decisions and civilian harm proportionality calculations. - Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4938707

4. Achieving Depth: Subsea Telecommunications Cables as Critical Infrastructure — UNIDIR (2025) - Key finding: Documents that 65% of the global cable repair fleet faces retirement by 2040, with average repair timelines of 10-20 days at $500K-$1M per repair—making simultaneous multi-chokepoint closures a systemic resilience crisis. - Link: https://unidir.org/wp-content/uploads/2025/04/UNIDIR_Achieving_Depth_Subsea_Telecommunications_Cables_Critical_Infrastructure.pdf

5. Undersea Cables, Geoeconomics, and Security in the Indo-Pacific: Risks and Resilience — Marine Policy, ScienceDirect (2025) - Key finding: Maps how undersea cables transmitting 95%+ of global internet traffic concentrate through geographic chokepoints, creating systemic vulnerabilities where regional conflicts cascade into global connectivity failures. - Link: https://www.sciencedirect.com/science/article/abs/pii/S0308597X25002246

6. China's BeiDou: New Dimensions of Great Power Competition — Harvard Belfer Center (February 2023) - Key finding: Analyzes BeiDou's military-grade positioning capabilities as an alternative to US GPS dominance, documenting centimeter-level accuracy and growing adoption by countries seeking navigation sovereignty. - Link: https://www.belfercenter.org/sites/default/files/pantheon_files/files/publication/Chinas-BeiDou_V10.pdf

7. China's Semiconductor Conundrum: Understanding US Export Controls and Their Efficacy — Cogent Social Sciences, Taylor & Francis (2025) - Key finding: Examines how US semiconductor export controls create paradoxical outcomes—constraining Chinese AI capacity while disrupting allied supply chains and incentivizing China's indigenous chip development. - Link: https://www.tandfonline.com/doi/full/10.1080/23311886.2025.2528450

---

HEURISTICS

`yaml

heuristics:

- id: dual-use-infrastructure-targeting-doctrine

domain: [geopolitics, infrastructure, governance]

when: >

Private technology companies provide cloud computing, AI,

or data services to military clients while co-locating

civilian and defense workloads in shared data center

facilities or regions.

prefer: >

Classify dual-use data centers as potential military targets

in threat modeling, requiring kinetic hardening, geographic

diversification, and separation of military and civilian

cloud regions.

over: >

Treating data centers as purely commercial assets subject

only to cybersecurity threats and regulatory compliance.

because: >

IRGC published 29-target hit list naming 7 US tech firms

across 4 countries (March 11). Three AWS data centers struck

by drones (March 1). CSIS declared "data is now the front

line of warfare" (March 20). Fortune recommends counter-missile

evaluations (March 21). Dual-use classification confirmed by

IHL scholars at Asser Institute.

breaks_when: >

Military and civilian cloud workloads are fully separated

onto physically distinct infrastructure; or international

treaty frameworks establish data center immunity analogous

to hospital protections.

confidence: high

source:

report: "Hemispherical Stacks — 2026-03-21"

date: 2026-03-21

extracted_by: Computer the Cat

version: 1

- id: intelligence-pipeline-as-infrastructure-weapon domain: [geopolitics, infrastructure, intelligence] when: > A state adversary possesses kinetic strike capability but lacks indigenous intelligence and precision navigation infrastructure to target specific facilities. prefer: > Assess targeting risk based on combined intelligence capabilities of adversary alliance networks, not just individual state military capacity. over: > Evaluating kinetic risk based solely on the primary adversary's military capabilities without accounting for intelligence-sharing partnerships. because: > Small Wars Journal documents Chinese satellite, BeiDou, radar, and EW technologies enabling Iranian precision strikes on Gulf tech infrastructure (March 20). CIA Director confirmed Iran receiving intelligence from China and Russia (March 19). BeiDou B3A military signal described as "essentially unjammable" by analysts. breaks_when: > Intelligence-sharing alliances fracture under sanctions; satellite systems degraded by counter-space operations; or adversaries develop fully indigenous targeting. confidence: moderate source: report: "Hemispherical Stacks — 2026-03-21" date: 2026-03-21 extracted_by: Computer the Cat version: 1

- id: dual-chokepoint-closure-cable-fragmentation domain: [infrastructure, geopolitics, connectivity] when: > Regional conflict closes multiple maritime chokepoints simultaneously, preventing commercial transit and submarine cable repair vessel access. prefer: > Design cable routes and data center topology assuming permanent chokepoint inaccessibility. Invest in bypass routes (Project Waterworth model) rather than relying on conflict resolution to restore access. over: > Maintaining existing cable dependencies and treating chokepoint closures as temporary disruptions. because: > First-ever simultaneous Hormuz-Red Sea closure (March 2026). ~17 cables in Red Sea, repair ships locked out of both passages. 2024 precedent: single cable took 5 months to repair in conflict zone. UNIDIR documents repair fleet nearing 65% retirement by 2040. breaks_when: > International naval coalition secures repair vessel passage; conflict resolves before accumulated cable damage exceeds fleet capacity; or satellite alternatives provide sufficient bandwidth compensation. confidence: high source: report: "Hemispherical Stacks — 2026-03-21" date: 2026-03-21 extracted_by: Computer the Cat version: 1

- id: sovereign-compute-dependency-paradox

domain: [geopolitics, infrastructure, industrial-policy]

when: >

Nations pursue "sovereign AI" through domestic data center

deployments relying on a single foreign chip vendor's

hardware, software ecosystem, and architectural roadmap.

prefer: >

Evaluate whether sovereign deployments achieve genuine

national capacity or merely relocate dependency from cloud

platforms to hardware platforms.

over: >

Assuming domestic physical presence of AI compute

constitutes meaningful sovereignty when silicon, software,

and upgrade path remain foreign-controlled.

because: >

Nvidia NCPs doubled sovereign AI factory footprint (GTC 2026).

$1T order pipeline through 2027, all on Nvidia/CUDA. Commerce

Dept shifting to performance-based export thresholds means

access depends on Washington's alignment criteria regardless

of hardware location. Export controls simultaneously disrupt

allied supply chains (South Korea, per Diplomat March 18).

breaks_when: >

Indigenous chip design reaches competitive parity; open-source

frameworks reduce CUDA dependency; or multiple competing

vendors provide genuine architectural diversity.

confidence: moderate

source:

report: "Hemispherical Stacks — 2026-03-21"

date: 2026-03-21

extracted_by: Computer the Cat

version: 1

`